Choosing Stripe, PayPal, or Braintree for app payments? This guide covers essential factors, challenges, and costs to help you make the right choice.

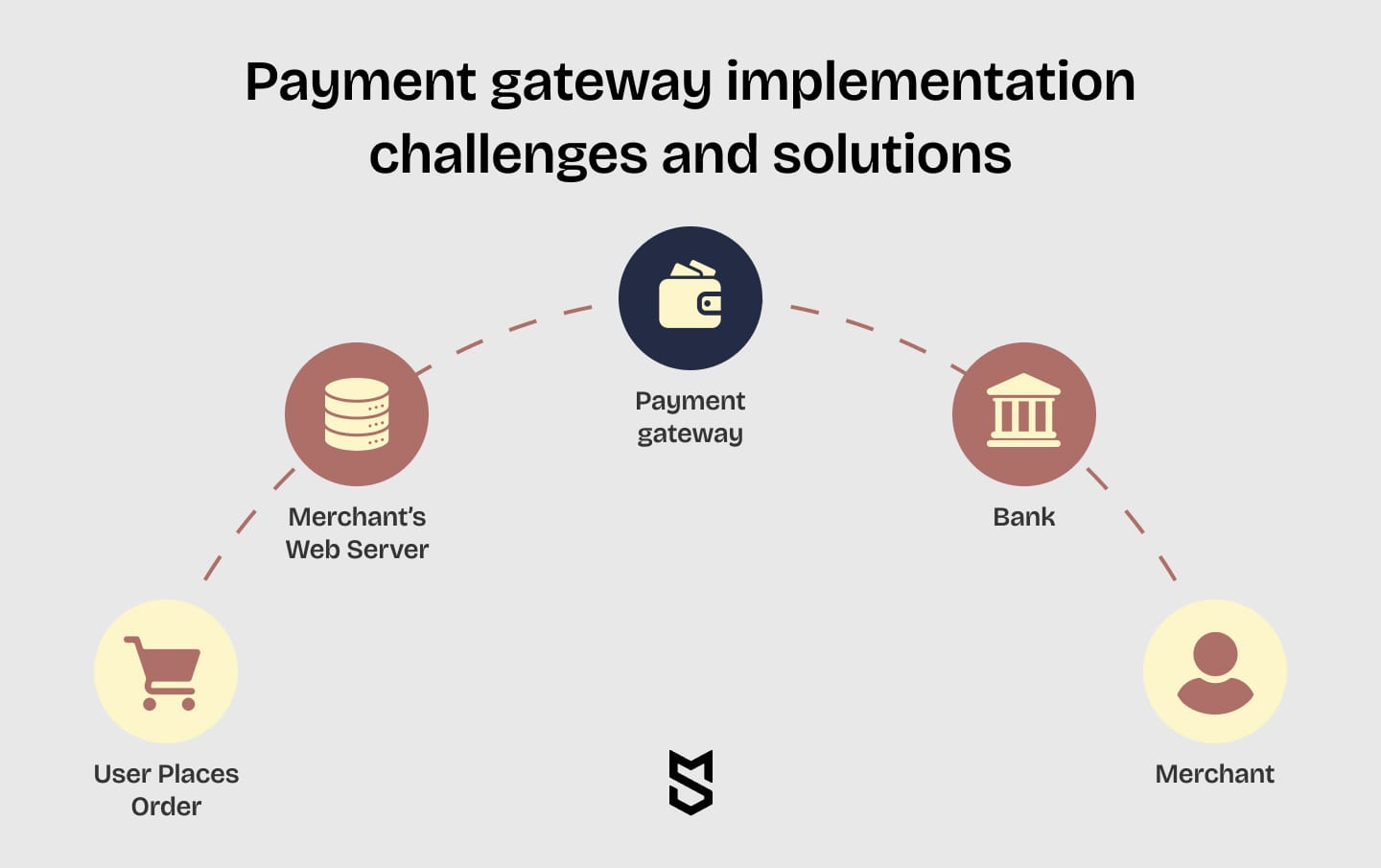

A payment gateway is essential for any business eyeing the mobile app market. Secure transmission of sensitive cardholder data is the responsibility of payment gateways, which are vital for facilitating online payments.

Which is the best payment service? Well, it depends. There are multiple options to select from, including PayPal, Braintree and Stripe. At Mind Studios, we'd like to share our ideas on the subject after successfully integrating numerous payment choices into multiple mobile apps — like James delivery, for example, which required payment options for admin, user, and customer applications. Curious about how to set up a secure, seamless payment experience in your app? Read on to get the inside information on making payments work smoothly for your business.

Highlights:

- Choosing the right payment gateway impacts processing speed, international payments, and user experience.

- Consider merchant account types: dedicated offers more control, and aggregate is faster to set up.

- Look at transaction fees carefully, as they vary significantly across different gateways.

What are payment gateways?

A payment gateway allows users to make payments quickly and securely. Whether for physical stores, online shops, or mobile apps, a payment gateway acts as an intermediary, sending transaction details to credit card processors or banks and returning authorization responses. You may have already faced some challenges in integrating a payment gateway firsthand. Below we will outline the main issues usually encountered by merchants and businesses during the integration process:

Challenges of payment gateway integration you need to consider

For business owners, choosing a payment gateway can feel like wandering through a maze. It’s not just about picking a brand you’ve heard of, like PayPal or Stripe. The way each platform handles payments, charges fees, and supports currencies can all have a big impact on your business’s bottom line. Here are some things to consider as you look through options:

- Transaction fees: Each gateway has its own fee structure, typically a mix of percentage and flat fees. For high-volume, small transactions, choosing a provider with volume discounts can help keep costs manageable.

- Currency support: If expanding globally, ensure your gateway handles multiple currencies well. Limited currency support can lead to extra costs or abandoned carts from customers who can’t pay in their local currency.

- Security features: Security essentials include fraud detection, encryption, and PCI compliance. Without these, you risk both financial loss and potential damage to your reputation.

Picking the wrong gateway might lead to slower payments, unexpected fees, or even issues processing international transactions — all of which add up over time and can strain your finances if not addressed properly. Needless to say, implementing a gateway isn’t always as easy as plug-and-play; without careful setup, you could lose money through failed transactions or authorization snags. As the main thing you should consider is a solid setup and testing process which makes a huge difference in keeping everything running smoothly.

At Mind Studios, we’ve integrated various payment systems like Stripe, PayPal, Authorize.net, and Braintree. We know the common pitfalls and how to avoid them, ensuring a seamless payment process that fits your business needs.

“There are 4 main aspects we and our clients take into account when choosing the right payment gateway to integrate: geographic specifics. For example, Stripe isn't available everywhere, and some of its features — such as Instant payouts — aren't available in some countries, fees and pricing structure, user experience, ease of integration and security and compliance.”

— Anton Baryshevskiy, Mind Studios Co-founder and Head of Business Development

Looking for guidance? Schedule a free consultation with our experts, and let us help you choose and implement the right payment gateway for your business.

Let’s explore tech

solutions

Get our expertise

What do you need to consider when choosing a mobile app payment gateway?

When it comes to choosing the right payment gateway for your app, several factors can make or break the experience for both you and your users. The right gateway will align with your business goals, secure transactions, and offer smooth processing. Here’s what you’ll want to consider:

- Merchant account type

- Security

- Pricing

- Customer experience

- International acceptance

Merchant account type

There are two types of merchant accounts: dedicated and aggregate. Here’s a small comparison for you to see the difference.

| Dedicated merchant account | Aggregate merchant account |

|---|---|

| A personal account set up by the provider for the merchant’s business transactions | A joint account setup by the aggregator that’s used by a number of merchants |

| Funds are deposited directly to your business’s bank account, and you control the process fully | Funds go through the aggregator and are checked by it, after which, if no suspicious activity is found, the money is deposited to your bank account |

| Fees are set separately for each account | Fees are fixed at the provider level and are the same for all merchants using the account |

| To setup a dedicated merchant account, the business and its owner go through a full check of credit and financial history, liabilities, reputation, etc. | Fairly easy to set up and requires little verification information |

| Takes time to set up due to all the checks | Setting up an account is quite fast |

| Transaction processing is fast, usually taking less than a day | Transaction processing can take up to 2–3 days |

| More expensive | Usually cheaper |

The differences between these two types of accounts are significant and the choice should be made with care.

- Full control with a dedicated account: With a dedicated account, you control every aspect of your transactions, including fees. This is ideal for larger businesses with high transaction volumes, where fixed aggregator fees can add up fast. Plus, dedicated accounts often offer faster transaction processing, with funds deposited to your account sooner.

- More setup requirements for dedicated accounts: If your business is new or has a few issues with its credit history, setting up a dedicated account may take time and effort. The extensive setup process includes financial checks that might not suit businesses starting out or those needing quick access to payment options.

- Easy setup with an aggregate account: Aggregate accounts require far less setup, need minimal information, and allow you to start accepting payments almost immediately. This option works well for businesses that need to go live quickly.

- Fraud risks with aggregate accounts: Since aggregate accounts group multiple businesses under one account, you risk being affected by fraudulent actions from other merchants. Aggregators keep a close eye on activity to prevent fraud, but account suspensions and fund holds can still occur if suspicious behavior is detected. However, there’s a way to avoid this: you can use a large aggregate account provider so that even an occasional criminal is not a big enough issue to close a whole account.

Also, it’s worth mentioning that among the payment systems for mobile apps, there are more reputable and trusted aggregators than dedicated account providers.

Mind Studios tip: Consider your growth trajectory when deciding between a dedicated and an aggregate account. A dedicated account offers more control and could save you money with high transaction volumes. However, an aggregate account might be the easiest way to accept payments quickly if you're just starting.

Security

As with everything that involves money transfers, security is the first and most important thing you should think about after you’ve made up your mind about the type of merchant account. In terms of making your app secure, you need to consider the following:

- Protecting sensitive financial data

Security involves safeguarding crucial customer details, like credit card numbers, expiration dates, and security codes (CVC2/CVV2), which require strong protection from unauthorized access and fraud. - Data encryption is essential

Encrypting sensitive information is necessary, ensuring that any data shared during transactions remains secure and out of reach for potential threats. - Industry standards for security

Reputable mobile payment systems adhere to the Payment Card Industry Data Security Standard (PCI DSS), a key framework that sets high-security requirements and helps guarantee the secure handling of financial information.

Mind Studios tip: Always choose a gateway that meets PCI DSS standards. It’s crucial to ensure your customers' financial data is protected. Look for additional security features like fraud detection and encryption to safeguard transactions further. You can read more about mobile payment security in our article.

Pricing

There are many pricing models among mobile payment gateways, and the rates can differ quite significantly. Here are the main points that you need to know about pricing when integrating a payment gateway:

- Monthly and per-transaction fees vary

Some providers include a monthly fee alongside per-transaction costs, while others skip the monthly charge. Costs will depend on service features, ease of use, and geographic reach. - Chargeback and refund fees

Additional fees often apply for handling chargebacks and refunds. The amount can differ, and not all providers refund fees when disputes resolve in favor of the merchant.

So, before you make a final decision as to which payment gateway to integrate, check that your company can handle the prices for the service in the long run.

Mind Studios tip: Look closely at all associated fees before choosing. Understanding the long-term costs of transaction fees, chargebacks, and monthly charges can help you avoid surprises, especially as your business scales.

Customer experience

When you start considering integrating payments into your app, consider which service will simplify the process. Here are the key things you need to know to improve your customers’ experience:

- Streamlined checkout process is essential

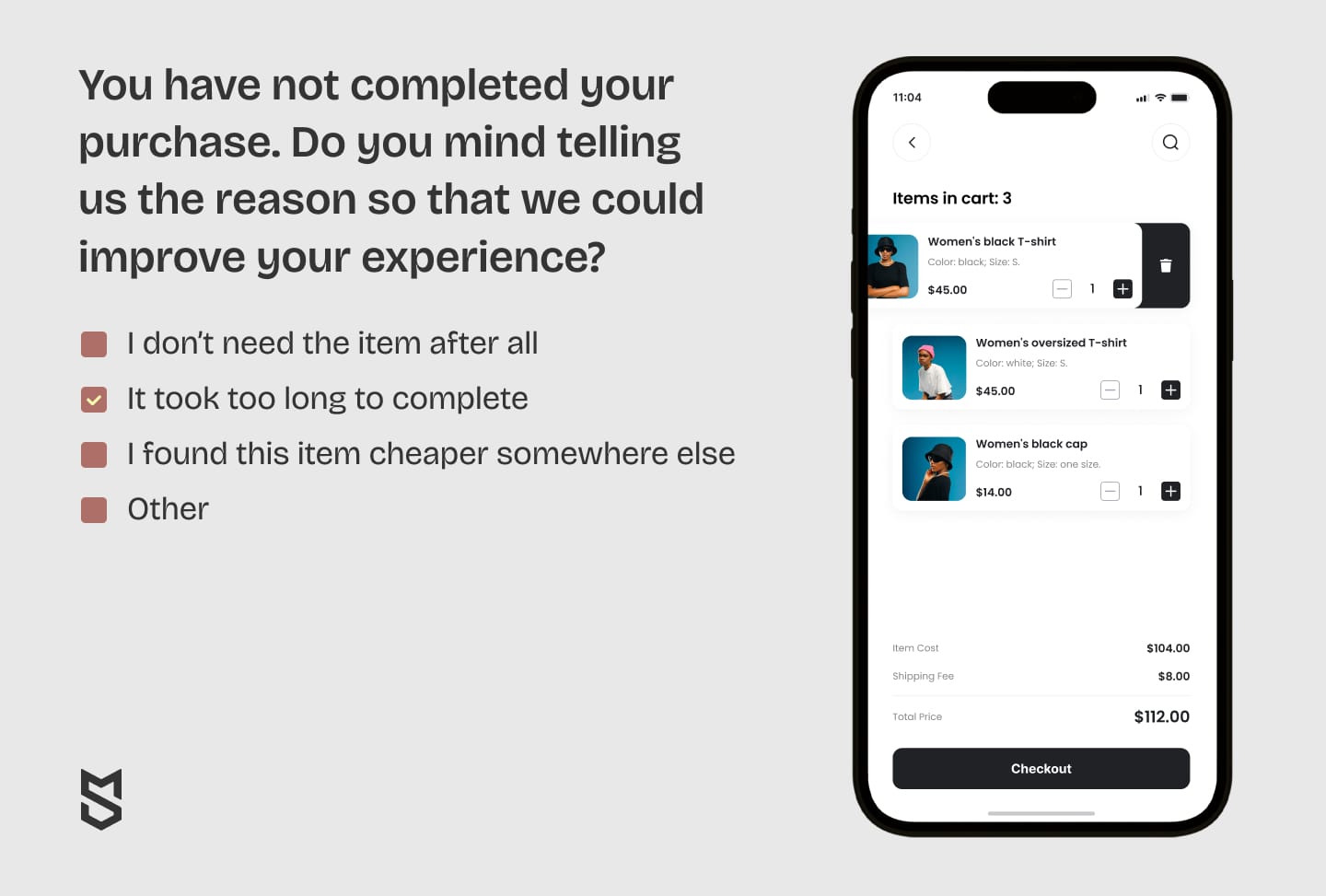

Customers shopping on mobile apps quickly abandon carts if checkout feels too lengthy or complicated. An easy, quick process keeps them engaged and reduces drop-off rates. In fact, a “too long and complicated process” was among the top three reasons for cart abandonment in 2024. - Diverse payment options to meet customer needs

Offering multiple payment methods — credit and debit cards, local payment options, Android Pay, Apple Pay, and even Bitcoin — ensures convenience for many customers and helps prevent cart abandonment.

Mind Studios tip: A smooth checkout process can make or break your sales. Opt for a payment gateway that supports multiple payment methods and ensures a quick, straightforward checkout. Remember, convenience is key to minimizing cart abandonment.

International acceptance

If your business primarily serves local customers, that’s a good start — but launching an app or website suggests you're gearing up for broader growth. For international reach, you’ll need a payment gateway that supports global transactions smoothly.

Mind Studios tip: Confirm that your chosen gateway can handle payments in each target market when preparing for cross-border expansion. Gateways vary in features and fees by region, so a bit of extra research now will go a long way to ensure a consistent, hassle-free experience for your customers abroad.

- Stripe supports businesses in over 40 countries. However, it may not support all features, such as instant payouts, in every region.

- PayPal operates in over 200 countries and regions, but specific features (like PayPal Pro or PayPal Credit) may not be available everywhere.

- Braintree, a PayPal service, is available in over 45 countries, but similar to Stripe, specific features may vary by region. So what is the difference between Braintree and PayPal? Braintree offers reduced rates and custom payment options for businesses with over $80,000 worth of transactions per month, whereas PayPal's discounts are scalable, allowing businesses to potentially save on fees as their sales increase.

Not every mobile payment integration gateway works in every country, but you might not need that, either. Look for the countries you already do business with first, then the countries you would like to expand into. The more countries there are on your gateway provider's list, the bigger your opportunities are. Always check the latest information on each provider’s website, as their availability can expand or contract depending on regulatory conditions.

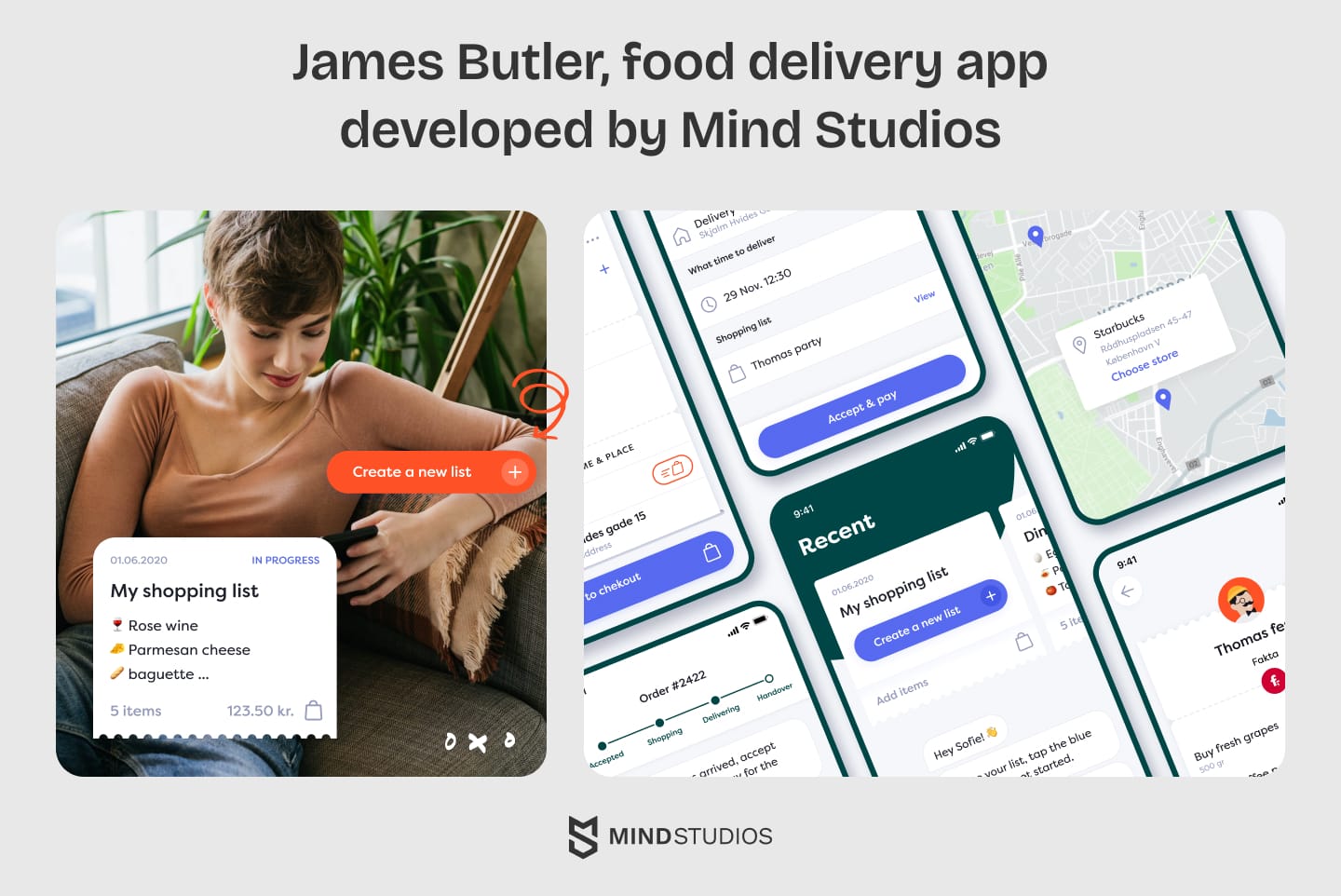

Mind Studios case: James delivery app

We’ve seen how payment gateway choices can make or break a project. While developing the James delivery app, we initially went with Stripe, but soon found that it didn’t support instant payments in Denmark — a key feature for their business model. With the launch just weeks away, this could have been a huge setback.

After consulting with the client, we pivoted to using SEPA via Danske Bank for instant payments. Though integrating SEPA required dealing with outdated XML formats and complex processes, we managed to get it up and running smoothly in time for launch.

This experience reinforced the importance of thoroughly researching gateway capabilities in every region before integration.

Selecting a payment gateway isn't just about plugging it into your app — it’s about making decisions that impact your business model, costs, and how your customers experience payments. Ready to elevate your payment processing? Learn how our team can integrate the best payment solution tailored to your business needs and ensure customers enjoy a seamless and secure checkout experience.

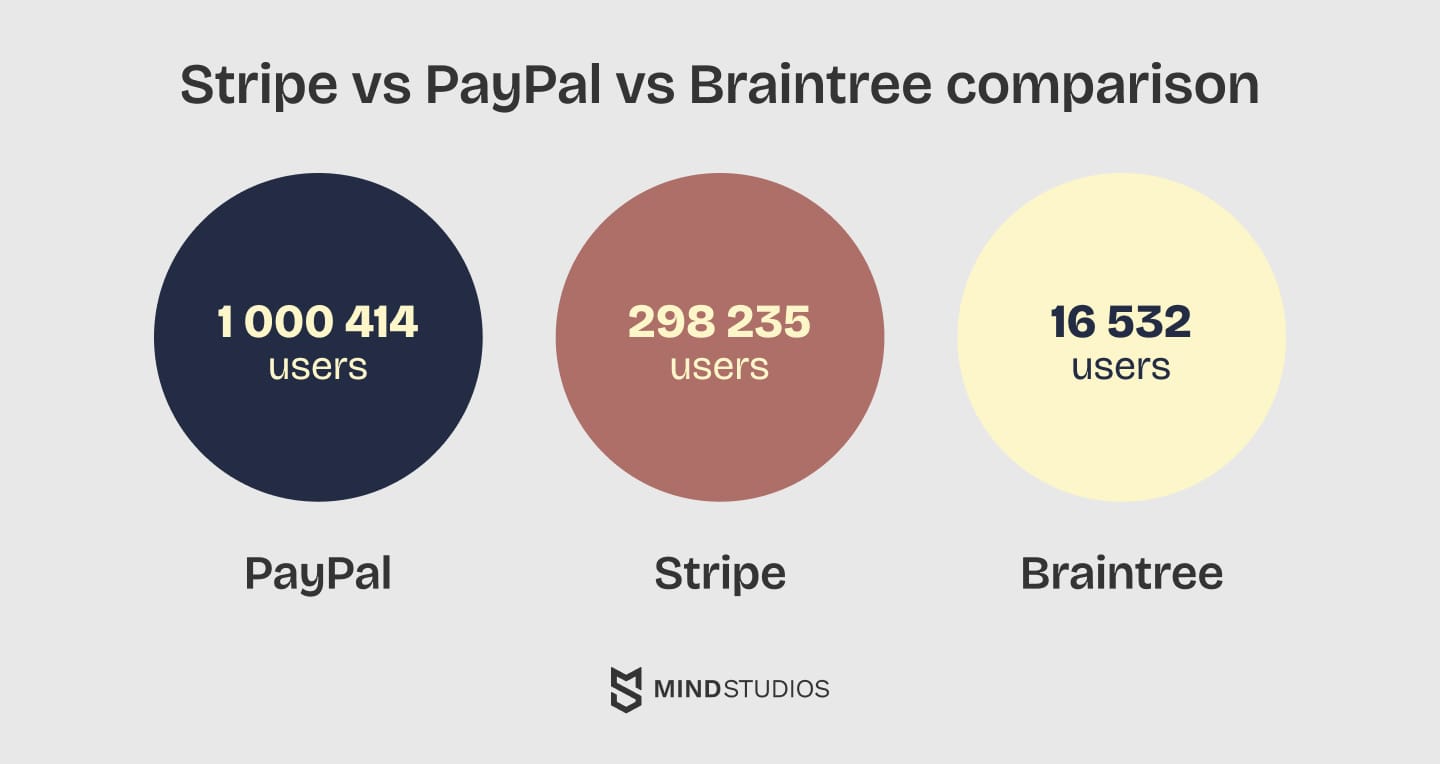

How to choose an integration service? Stripe vs PayPal vs Braintree

These three payment gateways are today’s top-tier services, mainly thanks to the high level of security they offer and the range of payment options they support. Basically, with any of these service providers you’ll be able to receive payments from Visa, Mastercard, American Express, JCB, and Discover credit and debit cards, a selection of local services (lists are provided on the websites), Apple Pay and Google Pay, and, of course, Bitcoin.

While there are a lot of similarities between Stripe, PayPal, and Braintree, there are also differences, which we’ll highlight below:

| Feature | Stripe | Paypal | Braintree |

|---|---|---|---|

| Ease of integration | Complex integration process. Requires technical expertise. | Moderate complexity; user-friendly for many but can be overwhelming. | Reasonable ease of use; some technical skills required. |

| Transaction fees | Higher fees, especially for international transactions. | Relatively high fees. Can add up for frequent users. | Competitive fees, especially for international transactions. |

| Currency support | Limited compared to competitors; fewer currencies available. | Supports fewer currencies and could limit global reach. | Strong currency support, better than PayPal. |

| Customization options | Highly customizable. Can be overwhelming for newcomers. | Limited customization options. More of a one-size-fits-all. | Some customization is available, but not as extensive as Stripe. |

| Global coverage | Limited to 46 countries, growing but still fewer than PayPal. | Extensive global presence. Well-known and trusted worldwide. | Good global reach, available in more countries than Stripe. |

| Adoption curve | Steeper learning curve: it may take time to master all features. | More straightforward for most users with a familiar interface. | Moderate learning curve; easier for those with tech experience. |

Stripe

Comparing PayPal vs Stripe, as these two are probably the closest rivals on the market, the biggest difference between PayPal and Stripe is that the latter has Stripe.js, a default script that allows your customers’ data to be sent directly to Stripe, bypassing your servers. This feature makes your mobile payment system integration automatically PCI-compliant and secure so that even if your servers are compromised, customer data is not there to be stolen.

Stripe was a game changer in several ways. They’re setting new standards for API protocols and tools and are pushing their competitors to follow. Even PayPal had to create new REST APIs to keep up.

Supported currencies: Supports over 135 currencies, allowing customers to pay in their local currency.

Fees:

- Domestic transactions: 2.9% + $0.30 per transaction in the U.S.

- International transactions: 1% additional fee for cross-border payments.

- In-person payments (Stripe Terminal): 2.7% + $0.05.

Stripe was created mainly for developers, so the biggest challenge would probably be the actual integration — if you’re not tech-savvy, you won’t be able to use all Stripe has to offer. That is unless you have a skilled team of developers working on your mobile app!

PayPal

What no one has yet to take away from PayPal is the title of the most popular mobile payment gateway integration system. True, Stripe is snapping at PayPal’s heels, but they still have some way to go. The reason is that PayPal has been on the market longer and is available in more than 200 countries. Furthermore, if you look around, many people worldwide (and many of your potential customers) already have and actively use PayPal accounts. They’re familiar with the system and find it easy to use.

Supported currencies: Limited to 25 currencies, which may limit international transactions compared to Braintree and Stripe.

Fees:

- Domestic transactions: 2.9% + $0.30 per transaction in the U.S.

- International transactions: Higher at 4.4% + a fixed fee based on currency.

- Chargebacks: $20 per incident.

- Instant Pay option: For an additional $0.25, money can appear in your account within half an hour, depending on card issuer policies.

PayPal processes payments faster than Stripe most of the time. Although they both state that payments will be processed in 2 to 3 business days, in reality, the money paid by your customers via PayPal has every chance of appearing on your bank account the next day under normal circumstances, while Stripe can, in fact, take a few days.

Don’t know how to choose the perfect fit for your integration? Schedule a free consultation with our team, and we’ll help you navigate the options to find the best payment solution for your business.

Braintree

Being a part of PayPal, Braintree is PayPal’s way of offering a middle ground of sorts. Braintree’s international fees, for example, are lower than those PayPal charges.

Supported currencies: Over 130 currencies for payments, with settlements in 44, providing extensive multicurrency support that’s ideal for international businesses.

Fees:

- Domestic transactions: 2.9% + $0.30 per transaction in the U.S.

- International transactions: Additional 1% fee.

- Chargebacks: $15 per incident.

If we imagine a Braintree vs Stripe battle, however, it would most probably end in a draw, as both mobile payment gateways have an approximately equal number of advantages:

- The number of supported currencies is almost the same: 130+ for Braintree and 135+ for Stripe

- Both offer a decent marketplace

But

- Braintree is available for merchants in more countries than Stripe

- Stripe is more customizable, while Braintree mostly offers a selection of templates

- Payments with Stripe Terminal are processed at lower rates

- Braintree accepts payments with Venmo and has smooth integration with PayPal

How much does it cost to integrate a payment gateway?

After analyzing the leading contenders, it's time to consider the price of incorporating a payment gateway into your mobile app. Each alternative has its own set of advantages and disadvantages, but understanding the cost of integration is critical for every firm.

Integrating a payment gateway is not a simple plug-and-play process. To provide your users with a smooth experience, you must invest in development time, skill, and careful planning. Costs vary depending on the extent of customization required, the complexity of your app, and the payment provider you choose. We've broken down the essential processes and associated costs of integrating a payment gateway into a mobile app.

| Development stage | Time, h | Cost, USD |

|---|---|---|

| Front-end development | 24–32 | 1080–1440 |

| Back-end development | 32–40 | 1440–1800 |

| QA and testing | 20–28 | 900–1260 |

| Deployment | 8–16 | 360–720 |

| Total | 84–116 | 3780–5220 |

While these estimations provide a general idea, the actual cost of integrating a payment gateway can vary based on your app's complexity, features, and scale. Any additional logic (for example, how customers are billed) is evaluated within the context of the overall project.

If you need a more tailored cost assessment, Mind Studios is here to help. Schedule a free consultation with our experts, and we’ll help you estimate the budget for integrating the right payment gateway into your mobile app.

Conclusion

As you can see, choosing a payment gateway for a mobile app can be a tricky business, with the differences so subtle they might seem insignificant at first glance. But those differences may be deal-breakers when you look deeper. Mobile app development with Mind Studios includes app payment system integration. We’ll offer insights from our previous projects and analysis and advice to help you find the gateway that fits your business and your app. If you have any questions, get in touch with our specialists.